Application Provision

1

Application and Definitions

1.1

1.2

In this Part the following definitions shall apply:

- (1) changes in its business, including:

- (a) the acute risk to earnings posed by falling or volatile income; and

- (b) the broader risk of a firm’s business model or strategy proving inappropriate due to macroeconomic, geopolitical, industry, regulatory or other factors; or

- (2) its remuneration policy.

- (a) who has relationship with A of the kind specified in s. 421 of FSMA;

- (b) who is a member of the same financial conglomerate as A;

- (c) who has a common management relationship with A;

- (d) who has a common management relationship with any person who falls into (a);

- (e) who is a subsidiary of a person in (c) or (d);

- (f) who is member of the same consolidation group as A; or

- (g) whose omission from an assessment of the risks to A of A's connection to any person coming within (a)-(f) or an assessment of the financial resources available to such persons would be misleading.

- (1) the risk to a firm caused by its contractual or other liabilities to or with respect to a pension scheme (whether established for its employees or those of a related company or otherwise); or

- (2) the risk that the firm will make payments or other contributions to or with respect to a pension scheme because of a moral obligation or because the firm considers that it needs to do so for some other reason.

1.3

- 01/01/2014

- Legal Instruments that change this rule 1.3

Export chapter as

2

Adequacy of Financial Resources

Overall financial adequacy rule

2.1

- 01/01/2014

- Legal Instruments that change this rule 2.1

3

Strategies, Processes and Systems

3.1

- (1) to assess and maintain on an ongoing basis the amounts, types and distribution of financial resources, own funds and internal capital that it considers adequate to cover:

- (a) the nature and level of the risks to which it is or might be exposed;

- (b) the risk in the overall financial adequacy rule in 2.1; and

- (c) the risk that the firm might not be able to meet the obligations in Part Three of the CRR in the future;

- (2) that enable it to identify and manage the major sources of risk referred to in (1) including the major sources of risk in each of the following categories where they are relevant to the firm given the nature and scale of its business:

- (a) credit and counterparty risk;

- (b) market risk;

- (c) liquidity risk;

- (d) operational risk;

- (e) concentration risk;

- (f) residual risk;

- (g) securitisation risk, including the risk that the own funds held by a firm in respect of assets which it has securitised are inadequate having regard to the economic substance of the transaction including the degree of risk transfer achieved;

- (h) business risk;

- (i) interest rate risk in the non-trading book;

- (j) risk of excessive leverage;

- (k) pension obligation risk; and

- (l) group risk.

- (3) to ensure that the firm's own funds can absorb potential losses resulting from stress scenarios, including those identified under the supervisory stress test.

[Note: Art 73 (part) and Art 104b (part) of the CRD]

3.2

- 01/01/2014

- Legal Instruments that change this rule 3.2

3.3

- 01/01/2014

- Legal Instruments that change this rule 3.3

3.4

A firm must:

- (1) carry out regularly the assessments required by the overall Pillar 2 rule in 3.1; and

- (2) carry out regularly assessments of the processes, strategies and systems required by the overall Pillar 2 rule in 3.1 to ensure they remain comprehensive and proportionate to the nature, scale and complexity of the firm’s activities.

[Note: Art 73 (part) of the CRD]

- 01/01/2014

- Legal Instruments that change this rule 3.4

3.5

- (1) make an assessment of the firm-wide impact of the risks identified in accordance with that rule, to which end a firm must aggregate the risks across its various business lines and units, taking appropriate account of any correlation between risks; and

- (2) take into account the stress tests that the firm is required to carry out under the general stress test and scenario analysis rule in 12.1 and any stress tests that the firm is required to carry out under the CRR.

- 01/01/2014

- Legal Instruments that change this rule 3.5

4

Credit and Counterparty Risk

4.1

- 01/01/2014

- Legal Instruments that change this rule 4.1

4.2

- (1) enable it to assess the credit risk of exposures to individual obligors, securities or securitisation positions and credit risk at the portfolio level;

- (2) do not rely solely or mechanistically on external credit ratings; and

- (3) where its own funds requirements under Part Three of the CRR are based on a rating by an ECAI or based on the fact that an exposure is unrated, enable the firm to consider other relevant information for assessing its allocation of financial resources and internal capital.

[Note: Art 79(b) of the CRD]

- 01/01/2014

- Legal Instruments that change this rule 4.2

4.3

- 01/01/2014

- Legal Instruments that change this rule 4.3

4.4

- 01/01/2014

- Legal Instruments that change this rule 4.4

Export chapter as

5

Residual Risk

5.1

- 01/01/2014

- Legal Instruments that change this rule 5.1

6

Concentration Risk

6.1

A firm must address and control, by means which include written policies and procedures, the concentration risk arising from:

- (1) exposures to each counterparty including central counterparties, groups of connected counterparties and counterparties in the same economic sector, geographic region or from the same activity or commodity;

- (2) the application of credit risk mitigation techniques; and

- (3) risks associated with large indirect credit exposures such as a single collateral issuer.

[Note: Art 81 of CRD]

- 01/01/2014

- Legal Instruments that change this rule 6.1

7

Securitisation Risk

7.1

A firm must evaluate and address through appropriate policies and procedures the risks arising from securitisation transactions in relation to which the firm is investor, originator or sponsor, including reputational risks, to ensure in particular that the economic substance of the transaction is fully reflected in risk assessment and management decisions.

[Note: Art 82(1) of CRD]

- 01/01/2014

- Legal Instruments that change this rule 7.1

7.2

[Note Art 82(2) of the CRD]

- 01/01/2014

- Legal Instruments that change this rule 7.2

8

Market Risk

8.1

- 01/01/2014

- Legal Instruments that change this rule 8.1

8.2

- 01/01/2014

- Legal Instruments that change this rule 8.2

8.3

- 01/01/2014

- Legal Instruments that change this rule 8.3

8.4

A firm which has, in calculating own funds requirements for position risk in accordance with Part Three, Title IV, Chapter 2 of the CRR, netted off its positions in one or more of the equities constituting a stock-index against one or more positions in the stock-index future or other stock-index product, must have adequate financial resources and internal capital to cover the basis risk of loss caused by the future's or other product's value not moving fully in line with that of its constituent equities.

- 01/01/2014

- Legal Instruments that change this rule 8.4

8.4A

A firm must have adequate internal capital where it holds opposite positions in stock-index futures which are not identical in respect of either their maturity or their composition or both.

- 30/03/2018

- Legal Instruments that change this rule 8.4A

8.5

- 01/01/2014

- Legal Instruments that change this rule 8.5

8.6

[Note: Art 98(4) of the CRD]

- 01/01/2014

- Legal Instruments that change this rule 8.6

9

Interest Risk Arising from Non-Trading Book Activities

General requirements

9.1

A firm must implement systems to identify, evaluate and manage the risk arising from potential changes in interest rates that affect a firm’s non-trading activities including the risks of such changes impacting either or both of the following:

- (1) the economic value of the firm's non-trading activities;

- (2) the earnings in respect of the firm's non-trading activities.

[Note: Art 84 of the CRD]

9.1A

A firm must in addition implement systems to monitor and assess credit spread risk in respect of its non-trading activities.

- 31/12/2021

- Legal Instruments that change this rule 9.1A

9.1B

As an alternative to implementing internal systems under 9.1(1), and only where appropriate to its nature, size and complexity as well as business activities and overall risk profile, a firm may elect to implement the standardised framework set out in 9.13 to 9.43 to identify, evaluate and manage the risk arising from potential changes in interest rates that affect the economic value of the firm’s non-trading activities.

- 31/12/2021

- Legal Instruments that change this rule 9.1B

9.1C

- 31/12/2021

- Legal Instruments that change this rule 9.1C

9.2

9.3

9.4

[Deleted.]

9.4A

A firm must regularly carry out an evaluation in respect of the interest rate shock scenarios in 9.7 and immediately notify the PRA if any evaluation under this rule indicates that, as a result of the application of the interest rate scenarios in 9.7, the EVE would decline by more than 15% of the sum of its common equity tier one capital and its additional tier one capital.

- 31/12/2021

- Legal Instruments that change this rule 9.4A

9.5

A firm must carry out the evaluation under 9.2 as frequently as necessary for it to be reasonably satisfied that it has at all times a sufficient understanding of the degree to which it is exposed to the risks referred to in 9.2 and the nature of that exposure. In any case it must carry out those evaluations no less frequently than once a year.

[Note: Art 98(5) of the CRD]

- 01/01/2014

- Legal Instruments that change this rule 9.5

9.6

A firm’s management body must oversee and approve the firm’s risk appetite and risk management framework for managing interest rate risk from non-trading book activities.

- 31/12/2021

- Legal Instruments that change this rule 9.6

Interest rate shock scenarios

9.7

For the purposes of the evaluation in 9.4A, a firm must apply the following prescribed interest rate scenarios to all material currencies as determined in 9.8:

scenario 0: current interest rates;

scenario 1: parallel shock up;

scenario 2: parallel shock down;

scenario 3: steepener shock (short rates down and long rates up);

scenario 4: flattener shock (short rates up and long rates down);

scenario 5: short rates shock up; and

scenario 6: short rates shock down.

- 31/12/2021

- Legal Instruments that change this rule 9.7

9.8

For the purposes of 9.7 and 9.15, a firm shall determine which currencies are material currencies using the following tests:

- (1) each currency that has non-trading book assets in that currency more than 5% of total non-trading book assets shall be a material currency;

- (2) where the sum of non-trading book assets in material currencies as identified under (1) does not exceed 90% of total non-trading book assets, a firm must select additional currencies to be deemed material currencies such that the sum of non-trading book assets in material currencies as identified under (1) and (2) is at least 90% of total nontrading book assets;

- (3) each currency that has non-trading book liabilities in that currency more than 5% of total non-trading book liabilities shall be a material currency; and

- (4) where the sum of non-trading book liabilities in material currencies as identified under (3) does not exceed 90% of total non-trading book liabilities, a firm must select additional currencies to be deemed material currencies such that the sum of nontrading book liabilities in material currencies as identified under (3) and (4) is at least 90% of total non-trading book liabilities.

- 31/12/2021

- Legal Instruments that change this rule 9.8

9.9

For the interest rate scenarios specified in 9.7, a firm shall determine the change to interest rates in accordance with the following formulae:

| for scenario 0: | ΔRc(tk) | = | 0 |

| for scenario 1: | ΔRc(tk) | = | + |

| for scenario 2: | ΔRc(tk) | = | — |

| for scenario 3: | ΔRc(tk) | = | —0.65 . |ΔRshort,c(tk)| + 0.9 . |ΔRlong,c(tk)| |

| for scenario 4: | ΔRc(tk) | = | +0.8 . |ΔRshort,c(tk)| — 0.6 . |ΔRlong,c(tk)| |

| for scenario 5: | ΔRc(tk) | = | +ΔRshort,c(tk) |

| for scenario 6: | ΔRc(tk) | = | —ΔRshort,c(tk) |

Where:

c = the index that denotes currency;

k = the index that denotes the buckets in accordance with Table 2 in 9.17 below;

tk = the bucket midpoint of bucket k, measured in years;

ΔRc(tk) = the change in interest rate at the point tk for currency c;

![]() = the prescribed parallel interest rate shock for currency c determined in accordance with column two of Table 1 in 9.11;

= the prescribed parallel interest rate shock for currency c determined in accordance with column two of Table 1 in 9.11;

ΔRshort,c(tk) = the change in short interest rate at the point tk for currency c determined in accordance with the formulae in 9.10; and

ΔRlong,c(tk) = the change in long interest rate at the point tk for currency c determined in accordance with the formulae in 9.10.

- 31/12/2021

- Legal Instruments that change this rule 9.9

9.10

For the purposes of 9.9, a firm shall determine the value of ΔRshort(tk) and ΔRlong(tk) in accordance with the following formulae:

- (1) for ΔRshort,c(tk): ΔRshort,c(tk) = +Rshort,c_ . e

- (2) for ΔRlong,c(tk): ΔRlong,c(tk) = +Rlong,c . (1 – e )

- Where:

- c = the index that denotes currency;

- k = the index that denotes the buckets in accordance with Table 2 in 9.17 below;

- e = the mathematical constant that is the base of the natural logarithm;

- x = 4;

- tk = the bucket midpoint of bucket k, measured in years;

- ΔRshort,c(tk) = the change in short interest rate at the point tk for currency c;

- ΔRlong,c(tk) = the change in long interest rate at the point tk for currency c;

= the prescribed short interest rate shock for currency c determined in accordance with column three of Table 1 in 9.11; and

= the prescribed short interest rate shock for currency c determined in accordance with column three of Table 1 in 9.11; and  = the prescribed long interest rate shock for currency c determined in accordance with column four of Table 1 in 9.11.

= the prescribed long interest rate shock for currency c determined in accordance with column four of Table 1 in 9.11.

- 31/12/2021

- Legal Instruments that change this rule 9.10

9.11

For the purposes of 9.9, the interest rate shock scenarios for individual currencies are those in Table 1 below:

Table 1. Specified size of interest rate shocks for each currency (bps)

| Currency | Parallel | Short | Long |

| ARS | 400 | 500 | 300 |

| AUD | 300 | 450 | 200 |

| BRL | 400 | 500 | 300 |

| CAD | 200 | 300 | 150 |

| CHF | 100 | 150 | 100 |

| CNY | 250 | 300 | 150 |

| EUR | 200 | 250 | 100 |

| GBP | 250 | 300 | 150 |

| HKD | 200 | 250 | 100 |

| IDR | 400 | 500 | 350 |

| INR | 400 | 500 | 300 |

| JPY | 100 | 100 | 100 |

| KRW | 300 | 400 | 200 |

| MXN | 400 | 500 | 300 |

| RUB | 400 | 500 | 300 |

| SAR | 200 | 300 | 150 |

| SEK | 200 | 300 | 150 |

| SGD | 150 | 200 | 100 |

| TRY | 400 | 500 | 300 |

| USD | 200 | 300 | 150 |

| ZAR | 400 | 500 | 300 |

- 31/12/2021

- Legal Instruments that change this rule 9.11

9.12

- 31/12/2021

- Legal Instruments that change this rule 9.12

Standardised Framework

Calculating Loss in Economic Value

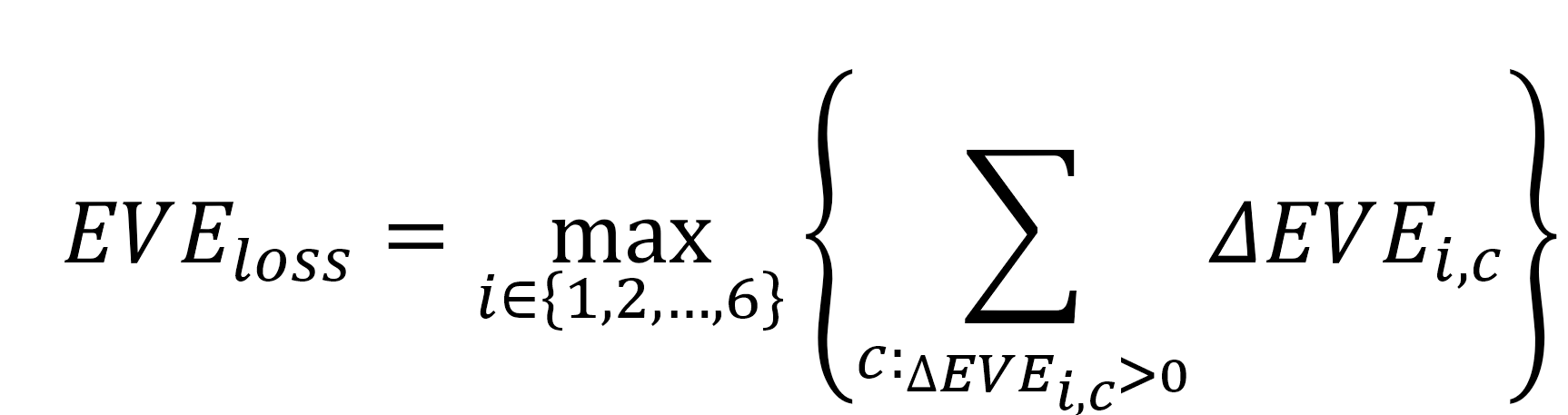

9.13

Using the standardised framework, a firm shall carry out the evaluation in 9.1(1) by calculating the loss in EVE (EV Eloss) in accordance with the following formula:

Where:

i = the index that denotes the interest rate shock scenarios in accordance with 9.15;

c = the index that denotes the material currencies in accordance with 9.15; and

ΔEV Ei,c = the change in economic value in currency c for interest rate scenario i as calculated in accordance with 9.14.

- 31/12/2021

- Legal Instruments that change this rule 9.13

9.14

For the purposes of 9.13, a firm must calculate the change in economic value in a given currency for a given interest rate scenario in accordance with the following formula:

ΔEV Ei,c = NA0i,c + KA0i,c

Where:

i = the index that denotes the interest rate shock scenarios in accordance with 9.15;

c = the index that denotes the material currencies in accordance with 9.15;

ΔEV Ei,c = the change in economic value in currency c for interest rate scenario i;

NA0i,c = the non-automatic option risk in currency c for interest rate scenario i as calculated in accordance with 9.16; and

KA0i,c = the automatic option risk in currency c for interest rate scenario i as calculated in accordance with 9.41.

- 31/12/2021

- Legal Instruments that change this rule 9.14

9.15

- 31/12/2021

- Legal Instruments that change this rule 9.15

9.16

For the purposes of 9.14, a firm must calculate the non-automatic option risk in currency c for interest rate scenario i (NA0i,c) in accordance with the following formula:

![]()

Where:

i = the index that denotes the interest rate shock scenarios in accordance with 9.15;

c = the index that denotes the material currencies in accordance with 9.15;

k = the index that denotes the buckets in accordance with Table 2 in 9.17;

DFi,c(tk) (respectively DF0,c(tk)) = the discount factor for bucket k in currency c for interest rate scenario i (respectively for interest rate scenario 0), calculated in accordance with 9.18; and

CFi,c(k) (respectively CF0,c(k)) = the net repricing cash flow for bucket k in currency c for interest rate scenario i (respectively for interest rate scenario 0), calculated in accordance with 9.19 to 9.40.

- 31/12/2021

- Legal Instruments that change this rule 9.16

9.17

For the calculation of discount factors and notional repricing cash flows in 9.18 and 9.19, a firm must project all notional repricing cashflows on to the following bucket intervals or bucket midpoints:

Table 2

| Time bucket intervals and mid points (M = months, Y = years) | |||

| Bucket number (k) | Bucket interval | Bucket midpoint | |

| Short-term rates | 1 | Overnight | 0.0028Y |

| 2 | > Overnight and <= 1M | 0.0147Y | |

| 3 | > 1M and <= 3M | 0.1667Y | |

| 4 | > 3M and <= 6M | 0.375Y | |

| 5 | > 6M and <= 9M | 0.625Y | |

| 6 | > 9M and <= 1Y | 0.875Y | |

| 7 | > 1Y and <= 1.5Y | 1.25Y | |

| 8 | > 1.5Y and <= 2 Y | 1.75Y | |

Medium-term rates |

9 | >2 Y and <= 3Y | 2.5Y |

| 10 | > 3Y and <= 4Y | 3.5Y | |

| 11 | > 4Y and <= 5Y | 4.5Y | |

| 12 | > 5Y and <= 6Y | 5.5Y | |

| 13 | > 6Y and <= 7Y | 6.5Y | |

Long-term rates |

14 | > 7Y and <= 8Y | 7.5Y |

| 15 | > 8Y and <= 9Y | 8.5Y | |

| 16 | >9 Y and <= 10Y | 9.5Y | |

| 17 | > 10Y and <= 15Y | 12.5Y | |

| 18 | > 15Y and <= 20Y | 17.5Y | |

| 19 | 20Y | 25Y | |

- 31/12/2021

- Legal Instruments that change this rule 9.17

9.18

- (1) For the purposes of 9.16, a firm must calculate the discount factor for bucket k in currency c for interest rate scenario i (DFi,c(tk)) in accordance with the following formula:

- Where:

- i = the index that denotes the interest rate shock scenarios in accordance with 9.15;

- c = the index that denotes the material currencies in accordance with 9.15;

- k = the index that denotes the buckets in accordance with Table 2 in 9.17;

- e = the mathematical constant that is the base of the natural logarithm;

- tk = the bucket midpoint of bucket k in accordance with Table 2 in 9.17; and

- Ri,c(tk)= subject to (2), the risk-free zero coupon rate at bucket midpoint tk in currency c for interest rate scenario i, including any commercial margin and other spread components.

- (2) A firm may elect to use the risk-free zero coupon rate Ri,c(tk) excluding commercial margin and other spread components, provided the firm either (i) implements a prudent and transparent methodology for deducting commercial margins and other spread components from the initial repricing cash flows CFα in 9.26 or (ii) determines that the effect of deducting commercial margins and other spread components is not material.

- 31/12/2021

- Legal Instruments that change this rule 9.18

9.19

In accordance with 9.21, 9.22, 9.23 and 9.24, a firm must assign each interest rate risk position arising from non-trading activities to one of the following categories:

category 1: automatic interest rate options;

category 2: non-maturing deposits;

category 3: fixed rate loans with retail borrowers that are subject to prepayment risk;

category 4: term deposits by retail depositors subject to early redemption risk; and

category 5: other positions.

- 31/12/2021

- Legal Instruments that change this rule 9.19

9.20

A firm must perform the allocation in 9.19 for all interest rate-sensitive non-trading book:

- (1) assets, excluding assets that are:

- (a) deducted from common equity tier one capital;

- (b) fixed assets, including real estate and intangible assets; or

- (c) equity exposures in the non-trading book;

- (2) liabilities, including all non-remunerated deposits and excluding common equity tier one capital; and

- (3) off-balance sheet items.

- 31/12/2021

- Legal Instruments that change this rule 9.20

9.21

Under 9.19, term deposits that satisfy either of the following conditions may be treated as other positions in 9.19:

- (1) the depositor has no legal right to withdraw the deposit; or

- (2) an early withdrawal results in a significant penalty that at least compensates for the loss of interest between the date of withdrawal and the contractual maturity date and the economic cost of breaking the contract.

- 31/12/2021

- Legal Instruments that change this rule 9.21

9.22

- 31/12/2021

- Legal Instruments that change this rule 9.22

9.23

- 31/12/2021

- Legal Instruments that change this rule 9.23

9.24

- 31/12/2021

- Legal Instruments that change this rule 9.24

9.25

- 31/12/2021

- Legal Instruments that change this rule 9.25

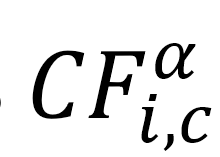

9.26

For each position, a firm must determine a set of initial repricing cash flows CFα as:

- (1) any repayment of principal;

- (2) any repricing of principal; and

- (3) any interest payment on a tranche of principal that has not yet been repaid or repriced.

- 31/12/2021

- Legal Instruments that change this rule 9.26

9.27

A firm must determine the set of initial repricing cash flows CFα for floating rate positions as:

- (1) a series of coupon payments until the next repricing; and

- (2) a par notional cash flow at the point of the next repricing.

- 31/12/2021

- Legal Instruments that change this rule 9.27

9.28

In accordance with 9.32 to 9.40 for each material currency c identified in accordance with 9.15 and for interest rate scenario i, a firm must allocate each notional repricing cash flow CFi,c to one of the buckets in Table 2 in 9.17 based on the repricing date, where repricing date means the date of each repayment, repricing or interest payment.

- 31/12/2021

- Legal Instruments that change this rule 9.28

9.29

- 31/12/2021

- Legal Instruments that change this rule 9.29

9.30

Where a firm chooses to apply the methodology in 9.29, that firm must:

- (1) split each initial repricing cash flow determined in 9.25, CFα such that:

- (a) the sum of the resulting two cash flows is equal to the initial repricing cash flow, CFα; and

- (b) the weighted average maturity of the resulting two cash flows equals the initial repricing cash flows’ maturity; and

- (2) document the methodology that the firm implements to split cash flows.

- 31/12/2021

- Legal Instruments that change this rule 9.30

9.31

- 31/12/2021

- Legal Instruments that change this rule 9.31

Non-maturing deposits

9.32

- 31/12/2021

- Legal Instruments that change this rule 9.32

9.33

For the purposes of 9.32(1) deposits made by small businesses, legal entities, sole proprietorships or partnerships managed as retail exposures provided the total aggregated liabilities are less than £877,000 may also be treated as retail deposits.

- 31/12/2021

- Legal Instruments that change this rule 9.33

9.34

For each category in 9.32, a firm must allocate each position to the following categories:

- (1) the core portion, consisting of deposits that are found to remain undrawn with a high degree of likelihood using data history of an appropriate length, and unlikely to reprice even under significant changes in the interest rate environment; and

- (2) the non-core portion, consisting of deposits not allocated to the core portion.

- 31/12/2021

- Legal Instruments that change this rule 9.34

9.35

For non-maturing deposits as determined in 9.34, the notional repricing cash flows in currency c for each interest rate scenario i, CFi,c, must be:

- (1) for the core portion, the initial notional repricing cash flows

in currency c for interest rate scenario i with the firm’s own estimates of tenors; and

in currency c for interest rate scenario i with the firm’s own estimates of tenors; and - (2) for the non-core portion, the initial notional repricing cash flows in currency c for interest rate scenario i with an overnight tenor.

- 31/12/2021

- Legal Instruments that change this rule 9.35

9.36

For the allocation in 9.34 and the calculation of CFi in 9.35, a firm must ensure that the proportion and average repricing date of core deposits is no greater than the caps in Table 3:

Table 3: Caps on core deposits

| Cap on proportion of core deposits (%) | Cap on average repricing date of core deposits (years) | |

| Transactional retail deposits (as referred to in 9.32(1)) | 90 | 5 |

| Other retail deposits (as referred to in 9.32(2)) | 70 | 4.5 |

| Other deposits (as referred to in 9.32(3)) | 50 | 4 |

- 31/12/2021

- Legal Instruments that change this rule 9.36

Fixed Rate Loans

9.37

For fixed rate loans with borrowers that are subject to prepayment risk as determined in 9.19, a firm must:

- (1) allocate each position to a single portfolio of homogeneous positions p denominated in a single currency c;

- (2) for each portfolio of homogeneous positions, determine and notify the PRA a baseline monthly conditional prepayment rate (

) in currency c under the current term structure of interest rates;

) in currency c under the current term structure of interest rates; - (3) for each portfolio of homogeneous positions, determine the conditional prepayment rate in currency c for interest rate scenario i, (CPRi,c) in accordance with the following formula:

![]()

- where γi refers to the prescribed scalar multiplier for each interest rate shock scenarios given in Table 4 below.

Table 4

| Scenario number i | Interest rate shock scenarios | γi (scenario multiplier) |

| 0 | Current interest rates | 1 |

| 1 | Parallel up | 0.8 |

| 2 | Parallel down | 1.2 |

| 3 | Steepener | 0.8 |

| 4 | Flattener | 1.2 |

| 5 | Short rate up | 0.8 |

| 6 | Short rate down | 1.2 |

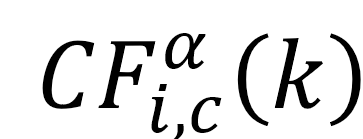

- (4) for each portfolio of homogeneous positions, determine the notional repricing cash flows CFi,c allocated to bucket 1 in accordance with Table 2 in 9.17, CFi,c(1), in accordance with the following formula:

![]()

- Where:

- (1) = the initial repricing cash flows CFα for interest rate scenario i with tenor that corresponds to bucket 1 in accordance with Table 2 in 9.17; and

- Ni(0)= the notional currently outstanding before any repayments.

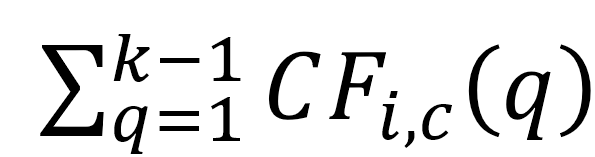

- (5) for each portfolio of homogeneous positions, determine the notional repricing cash flows CFi,c allocated to each bucket k in Table 2 where k > 1, CFi,c(k), in accordance with the following recursive formula:

- Where:

- k = the index that denotes the buckets in accordance with Table 2 in 9.17;

- W(k) = the width of bucket k measured in months and capped at 1200;

= the initial repricing cash flows CFα in currency c for interest rate scenario i with tenor that corresponds to bucket k;

= the initial repricing cash flows CFα in currency c for interest rate scenario i with tenor that corresponds to bucket k; - N(k – 1) = the notional outstanding after notional repricing cash flows in bucket k− 1 have transpired; and

= the sum of CFi determined for preceding buckets 1 to k − 1 .

= the sum of CFi determined for preceding buckets 1 to k − 1 .

- 31/12/2021

- Legal Instruments that change this rule 9.37

9.38

For the purpose of 9.37, firms may adjust the formulas in 9.37 (4) and (5) to reflect a base monthly conditional prepayment rate![]() that varies over the life of each loan in the portfolio. In that case, it is denoted as for each time bucket k or time bucket midpoint tk in accordance with Table 2 in 9.17.

that varies over the life of each loan in the portfolio. In that case, it is denoted as for each time bucket k or time bucket midpoint tk in accordance with Table 2 in 9.17.

- 31/12/2021

- Legal Instruments that change this rule 9.38

Term Deposits Subject to Early Redemption Risk

9.39

For term deposits by depositors subject to early redemption risk as determined in 9.19, a firm must:

- (1) allocate each position to a single portfolio of homogeneous positions p denominated in each material currency c;

- (2) for each portfolio of homogeneous positions, determine and notify the PRA a baseline term deposit redemption ratio

in currency c under the current term structure of interest rates;

in currency c under the current term structure of interest rates; - (3) for each portfolio of homogeneous loans, determine the conditional term deposit redemption ratio in currency c for interest rate scenario i,

in accordance with the following formula:

in accordance with the following formula:

![]()

- where ui refers to the prescribed scalar multiplier for each interest rate shock scenarios given in Table 5 below.

Table 5.

| Scenario number (i) | Interest rate shock scenarios | ui (scenario multiplier |

| 0 | Current interest rates | 1 |

| 1 | Parallel up | 1.2 |

| 2 | Parallel down | 0.8 |

| 3 | Steepener | 0.8 |

| 4 | Flattener | 1.2 |

| 5 | Short rate up | 1.2 |

| 6 | Short rate down | 0.8 |

- (4) for each portfolio of homogeneous positions, determine the notional repricing cash flows CFi,c allocated to bucket 1 in Table 2 in 9.17, CFi,c(1), in accordance with the following formula:

- Where:

-

= the initial repricing cash flows

= the initial repricing cash flows in currency c for interest rate scenario i with tenor that corresponds to bucket 1 in accordance with Table 2 in 9.17; and

in currency c for interest rate scenario i with tenor that corresponds to bucket 1 in accordance with Table 2 in 9.17; and - TDc = the total term deposits subject to early redemption for currency c.

- (5) for each portfolio of homogeneous positions, determine the notional repricing cash flows CFi allocated to bucket k in Table 2 other than bucket CFi(k), in accordance with the following formula:

![]()

- Where:

- k = the index that denotes the buckets in accordance with Table 2 in 9.17; and

- = the initial repricing cash flows in currency c for interest rate scenario i with tenor that corresponds to bucket k.

- 31/12/2021

- Legal Instruments that change this rule 9.39

Other positions

9.40

For other positions as determined in 9.19, a firm must determine the notional repricing cash flows CFi,c allocated to bucket k in Table 2 other than bucket 1, CFi(k), in accordance with the following formula:

![]()

Where:

k = the index that denotes the buckets in accordance with Table 2 in 9.17; and

![]() = the initial repricing cash flows

= the initial repricing cash flows![]() in currency c for interest rate scenario i with tenor that corresponds to bucket k.

in currency c for interest rate scenario i with tenor that corresponds to bucket k.

- 31/12/2021

- Legal Instruments that change this rule 9.40

Automatic interest rate options

9.41

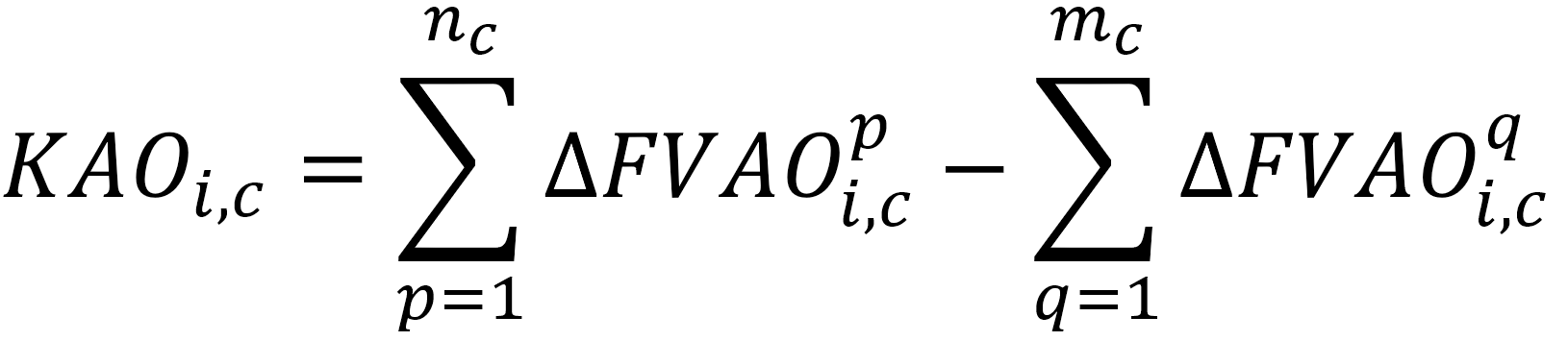

For 9.14, and subject to 9.42, a firm must determine the automatic option risk in currency c for interest rate scenario i (KA0i,c) for all automatic interest rate options as determined in 9.19 and 9.22 in accordance with the following formula:

Where:

nc = the index that denotes the number of all sold automatic options in currency c;

mc = the index that denotes the number of all bought automatic options in currency c;

![]() = the change in value of sold automatic option p for interest rate scenario i, calculated in accordance with 9.43; and

= the change in value of sold automatic option p for interest rate scenario i, calculated in accordance with 9.43; and

![]() = the change in value of bought automatic option q for interest rate scenario i, calculated in accordance with 9.43.

= the change in value of bought automatic option q for interest rate scenario i, calculated in accordance with 9.43.

- 31/12/2021

- Legal Instruments that change this rule 9.41

9.42

A firm may choose to include in the calculation of ![]() only bought automatic options that are used for hedging sold automatic interest rate options, provided that the firm must add to KA0i,c in 9.41 the value of bought automatic options that are not for hedging sold automatic interest rate options that is included in the firm’s own funds.

only bought automatic options that are used for hedging sold automatic interest rate options, provided that the firm must add to KA0i,c in 9.41 the value of bought automatic options that are not for hedging sold automatic interest rate options that is included in the firm’s own funds.

- 31/12/2021

- Legal Instruments that change this rule 9.42

9.43

- (1) For 9.41, a firm must calculate the change in value of sold automatic option p (respectively bought automatic option q) for interest rate scenario i other than interest rate scenario

(respectively

(respectively  ), as the increase in value of the option to the option holder:

), as the increase in value of the option to the option holder: - (a) from the value of the option for interest rate scenario 0; and

- (b) to the value of the option for interest rate shock scenario i with a relative increase in implied volatility of 25%.

- (2) For 9.41, a firm must set the change in value of sold automatic option p (respectively bought automatic option q) for interest rate scenario

(respectively

(respectively ), as 0.

), as 0. - (3) A firm must notify the PRA of the methodology used to estimate the value of automatic options in (1).

- 31/12/2021

- Legal Instruments that change this rule 9.43

10

Operational Risk

10.1

[Note: Art 85(1) of the CRD]

10.2

- 01/01/2014

- Legal Instruments that change this rule 10.2

11

Risk of Excessive Leverage

11.1

- 01/01/2014

- Legal Instruments that change this rule 11.1

11.2

[Note: Art 87(1) of the CRD]

11.3

[Note: Art 87(2) of the CRD]

- 01/01/2014

- Legal Instruments that change this rule 11.3

Export chapter as

12

Stress Tests and Scenario Analysis

12.1

- 01/01/2014

- Legal Instruments that change this rule 12.1

12.2

- (a) circumstances and events occurring over a protracted period of time;

- (b) sudden and severe events, such as market shocks or other similar events; and

- (c) some combination of the circumstances and events described in (a) and (b), which may include a sudden and severe market event followed by an economic recession.

- 01/01/2014

- Legal Instruments that change this rule 12.2

12.3

- 01/01/2014

- Legal Instruments that change this rule 12.3

12.4

- 01/01/2014

- Legal Instruments that change this rule 12.4

13

Documentation of Risk Assessments

13.1

- (a) the major sources of risk identified in accordance with the overall Pillar 2 rule in 3.1;

- (b) how it intends to deal with those risks; and

- (c) details of the stress tests and scenario analyses carried out, including any assumptions made in relation to scenario design, and the resulting financial resources estimated to be required in accordance with the general stress test and scenario analysis rule in 12.1.

- 01/01/2014

- Legal Instruments that change this rule 13.2

14

Application of this Part on an Individual Basis, a Consolidated Basis and a Sub-Consolidated Basis

14.1

- 01/01/2014

- Legal Instruments that change this rule 14.1

14.2

[Note: Art 108(1) of the CRD]

- 01/01/2014

- Legal Instruments that change this rule 14.2

14.2A

If the ICAAP rules apply to a firm on an individual basis, the firm must comply with the ICAAP rules to the same extent and in the same manner as it is required to comply with the obligations laid down in Parts Two to Four and Part Seven of the CRR.

14.3

14.4

14.4A

A PRA approved parent holding company or a PRA designated parent holding company must comply with the ICAAP rules on the basis of its consolidated situation and a PRA designated intermediate holding company or a PRA designated institution responsible for meeting CRR requirements on a consolidated basis must comply with the ICAAP rules on the basis of the consolidated situation of its UK parent financial holding company or UK parent mixed financial holding company.

14.4B

A PRA designated institution controlled by a UK parent financial holding company or a UK parent mixed financial holding company must comply with the ICAAP rules on the basis of the consolidated situation of that holding company, if the PRA is responsible for supervision of the firm on a consolidated basis.

[Note: Art 108(2) of the CRD]

14.5

14.6

14.7

- (1) the Article 109 undertaking must ensure that the consolidation group or sub-consolidation group has the processes, strategies and systems required by the overall Pillar 2 rule in 3.1;

- (2) the risks to which the overall Pillar 2 rule in 3.1 and the general stress test and scenario analysis rule refer are those risks as they apply to each member of the consolidation group;

- (3) the reference in the overall Pillar 2 rule in 3.1 to amounts and types of financial resources, own funds and internal capital (referred to in this rule as resources) must be read as being to the amounts and types that the Article 109 undertaking considers should be held by the members of the consolidation group or sub-consolidation group;

- (4) other references to resources must be read as being to resources of the members of the consolidation group or sub-consolidation group;

- (5) the reference in the overall Pillar 2 rule in 3.1 to the distribution of resources must be read as including a reference to the distribution between members of the consolidation group;

- (6) the reference in the overall Pillar 2 rule in 3.1 to the overall financial adequacy rule in 2.1 must be read as being to that rule as adjusted under 14.14-14.16 (level of application of the overall financial adequacy rule);

- (7) an Article 109 undertaking must be able to explain how it has aggregated the risks referred to in the overall Pillar 2 rule in 3.1 and the financial resources, own funds and internal capital required by each member of the consolidation group or sub-consolidation group; and

- (8) in particular, to the extent that the transferability of resources affects the assessment in (2), an Article 109 undertaking must be able to explain how it has satisfied itself that resources are transferable between members of the group in question in the stressed cases and the scenarios referred to in the general stress test and scenario analysis rule in 12.1.

14.8

14.9

14.10

- (a) takes into account the nature, level and distribution of the risks between all entities within the consolidated group or sub-consolidation group; and

- (b) ensures the amount allocated to each Article 109 undertaking adequately reflects the risks to which that Article 109 undertaking is exposed on an individual basis.

14.11

[Note: Art 109(1) (part) of the CRD]

14.12

14.12A

Where a firm, a PRA approved intermediate holding company, a PRA designated intermediate holding company, a PRA designated parent holding company or a PRA designated institution is responsible for meeting CRR requirements on a sub-consolidated basis, it must ensure that the risk management processes and internal control mechanisms at the level of the sub-consolidation group of which it is a member meet the standards set out in the risk control rules on a sub-consolidated basis.

14.13

[Note: Art 109(2) (part) of the CRD]

14.14

14.15

14.16

15

Reverse Stress Testing

15.1

This Chapter applies to a CRR firm.

- 03/08/2015

- Legal Instruments that change this rule 15.1

15.2

As part of its business planning and risk management obligations, including under the Risk Control Part of the PRA Rulebook, a firm must reverse stress test its business plan; that is, it must carry out stress tests and scenario analyses that test its business plan to failure. To that end, the firm must:

- (1) identify a range of adverse circumstances which would cause its business plan to become unviable and assess the likelihood that such events could crystallise; and

- (2) where those tests reveal a risk of business failure that is unacceptably high when considered against the firm's risk appetite or tolerance, adopt effective arrangements, processes, systems or other measures to prevent or mitigate that risk.

- 03/08/2015

- Legal Instruments that change this rule 15.2

15.3

Where the firm is a member of a UK consolidation group it must conduct the reverse stress test on an individual basis as well as on a consolidated basis in relation to the UK consolidation group.

15.4

The design and results of a firm's reverse stress test must be documented and reviewed and approved at least annually by the firm's senior management or governing body. A firm must update its reverse stress test more frequently if it is appropriate to do so in the light of substantial changes in the market or in macroeconomic conditions.

- 03/08/2015

- Legal Instruments that change this rule 15.4