INSPRU 1

Capital resources requirements and technical provisions for insurance business

INSPRU 1.1

Application

- 31/12/2006

INSPRU 1.1.1

See Notes

- 31/12/2006

INSPRU 1.1.2

See Notes

- 31/12/2006

INSPRU 1.1.3

See Notes

- 31/12/2006

INSPRU 1.1.4

See Notes

- 31/12/2006

INSPRU 1.1.5

See Notes

- 31/12/2006

INSPRU 1.1.6

See Notes

- 31/12/2006

Purpose

INSPRU 1.1.7

See Notes

- 31/12/2006

INSPRU 1.1.8

See Notes

- 31/12/2006

INSPRU 1.1.9

See Notes

- 31/12/2006

INSPRU 1.1.10

See Notes

- 31/12/2006

INSPRU 1.1.11

See Notes

- 31/12/2006

Establishing technical provisions

INSPRU 1.1.12

See Notes

- 31/12/2006

INSPRU 1.1.13

See Notes

- 31/12/2006

INSPRU 1.1.14

See Notes

- 31/12/2006

INSPRU 1.1.15

See Notes

- 31/12/2006

INSPRU 1.1.16

See Notes

- 31/12/2006

INSPRU 1.1.17

See Notes

- 31/12/2006

INSPRU 1.1.18

See Notes

- 31/12/2006

INSPRU 1.1.19

See Notes

- 31/12/2006

Reinsurance and analogous non-reinsurance financing agreements: risk transfer principle

INSPRU 1.1.19A

See Notes

- 31/12/2006

INSPRU 1.1.19B

See Notes

- 31/12/2006

INSPRU 1.1.19C

See Notes

- 31/12/2006

INSPRU 1.1.19D

See Notes

- 31/12/2006

INSPRU 1.1.19E

See Notes

- 31/12/2006

INSPRU 1.1.19F

See Notes

- 31/12/2006

Assets of a value sufficient to cover technical provisions and other liabilities

INSPRU 1.1.20

See Notes

- 31/12/2006

INSPRU 1.1.21

See Notes

- 31/12/2006

INSPRU 1.1.22

See Notes

- 31/12/2006

INSPRU 1.1.23

See Notes

- 31/12/2006

INSPRU 1.1.24

See Notes

- 31/12/2006

INSPRU 1.1.25

See Notes

- 31/12/2006

INSPRU 1.1.26

See Notes

- 31/12/2006

INSPRU 1.1.27

See Notes

- 31/12/2006

INSPRU 1.1.28

See Notes

- 31/12/2006

INSPRU 1.1.29

See Notes

- 31/12/2006

Localisation (UK firms only)

INSPRU 1.1.30

See Notes

- 31/12/2006

INSPRU 1.1.31

See Notes

- 31/12/2006

INSPRU 1.1.32

See Notes

- 31/12/2006

INSPRU 1.1.33

See Notes

- 31/12/2006

Matching of assets and liabilities

INSPRU 1.1.34

See Notes

- 31/12/2006

INSPRU 1.1.34A

See Notes

- 31/12/2006

INSPRU 1.1.35

See Notes

- 31/12/2006

INSPRU 1.1.36

See Notes

- 31/12/2006

INSPRU 1.1.37

See Notes

- 31/12/2006

INSPRU 1.1.38

See Notes

- 31/12/2006

INSPRU 1.1.39

See Notes

- 31/12/2006

INSPRU 1.1.40

See Notes

- 31/12/2006

Premiums for new business

INSPRU 1.1.41

See Notes

- 31/12/2006

INSPRU 1.1.42

See Notes

- 31/12/2006

Capital requirements for insurers

INSPRU 1.1.43

See Notes

- 31/12/2006

General insurance capital requirement

INSPRU 1.1.44

See Notes

- 31/12/2006

The premiums amount

INSPRU 1.1.45

See Notes

- 31/12/2006

INSPRU 1.1.46

See Notes

- 31/12/2006

The claims amount

INSPRU 1.1.47

See Notes

- 31/12/2006

INSPRU 1.1.48

See Notes

- 31/12/2006

INSPRU 1.1.49

See Notes

- 31/12/2006

INSPRU 1.1.50

See Notes

- 31/12/2006

The brought forward amount

INSPRU 1.1.51

See Notes

- 31/12/2006

INSPRU 1.1.52

See Notes

- 31/12/2006

INSPRU 1.1.53

See Notes

- 31/12/2006

Reinsurance ratio used in calculating the premiums amount and the claims amount

INSPRU 1.1.54

See Notes

- 31/12/2006

INSPRU 1.1.54A

See Notes

- 31/12/2006

INSPRU 1.1.55

See Notes

- 31/12/2006

Gross adjusted premiums amount used in calculating the premiums amount

INSPRU 1.1.56

See Notes

- 31/12/2006

INSPRU 1.1.57

See Notes

- 31/12/2006

INSPRU 1.1.58

See Notes

- 31/12/2006

INSPRU 1.1.59

See Notes

- 31/12/2006

Gross adjusted claims amount used in calculating the claims amount

INSPRU 1.1.60

See Notes

- 31/12/2006

INSPRU 1.1.61

See Notes

- 31/12/2006

INSPRU 1.1.62

See Notes

- 31/12/2006

INSPRU 1.1.63

See Notes

- 31/12/2006

INSPRU 1.1.64

See Notes

- 31/12/2006

INSPRU 1.1.65

See Notes

- 31/12/2006

Accounting for premiums and claims

INSPRU 1.1.66

See Notes

- 31/12/2006

INSPRU 1.1.67

See Notes

- 31/12/2006

INSPRU 1.1.68

See Notes

- 31/12/2006

INSPRU 1.1.69

See Notes

- 31/12/2006

INSPRU 1.1.70

See Notes

- 31/12/2006

INSPRU 1.1.71

See Notes

- 31/12/2006

Actuarial health insurance

INSPRU 1.1.72

See Notes

- 31/12/2006

Enhanced capital requirement for general insurance business

INSPRU 1.1.72A

See Notes

- 31/12/2006

INSPRU 1.1.72B

See Notes

- 31/12/2006

INSPRU 1.1.72C

See Notes

- 31/12/2006

INSPRU 1.1.72D

See Notes

- 31/12/2006

Insurance-related capital requirement

INSPRU 1.1.73

See Notes

- 31/12/2006

INSPRU 1.1.74

See Notes

- 31/12/2006

INSPRU 1.1.75

See Notes

- 31/12/2006

Calculation of the insurance-related capital requirement

INSPRU 1.1.76

See Notes

- 31/12/2006

INSPRU 1.1.77

See Notes

- 31/12/2006

INSPRU 1.1.78

See Notes

- 31/12/2006

INSPRU 1.1.79

See Notes

| Class of Business | Net Written Premium capital charge factor | Technical provision capital charge factor |

| Reporting Group: Direct and facultative business | ||

| Direct and facultative accident and health | 5.0% | 7.5% |

| Direct and facultative personal lines motor business | 10.0% | 9.0% |

| Direct and facultative household and domestic all risks | 10.0% | 10.0% |

| Direct and facultative personal lines financial loss | 25.0% | 14.0% |

| Direct and facultative commercial motor business | 10.0% | 9.0% |

| Direct and facultative commercial lines property | 10.0% | 10.0% |

| Direct and facultative commercial lines liability | 14.0% | 14.0% |

| Direct and facultative commercial lines financial loss | 25.0% | 14.0% |

| Direct and facultative aviation | 32.0% | 14.0% |

| Direct and facultative marine | 22.0% | 17.0% |

| Direct and facultative goods in transit | 12.0% | 14.0% |

| Direct and facultative miscellaneous | 25.0% | 14.0% |

| Reporting Group: Non-Proportional Treaty | ||

| Non-proportional accident & health | 35.0% | 16.0% |

| Non-proportional motor | 10.0% | 14.0% |

| Non-proportional transport | 16.0% | 15.0% |

| Non-proportional aviation | 61.0% | 16.0% |

| Non-proportional marine | 38.0% | 17.0% |

| Non-proportional property | 53.0% | 12.0% |

| Non-proportional liability (non-motor) | 14.0% | 14.0% |

| Non-proportional financial lines | 39.0% | 14.0% |

| Non-proportional aggregate cover | 53.0% | 12.0% |

| Reporting Group: Proportional Treaty | ||

| Proportional accident & health | 12.0% | 16.0% |

| Proportional motor | 10.0% | 12.0% |

| Proportional transport | 12.0% | 15.0% |

| Proportional aviation | 33.0% | 16.0% |

| Proportional marine | 22.0% | 17.0% |

| Proportional property | 23.0% | 12.0% |

| Proportional liability (non-motor) | 14.0% | 14.0% |

| Proportional financial lines | 25.0% | 14.0% |

| Proportional aggregate cover | 23.0% | 12.0% |

| Reporting Group: Miscellaneous Reinsurance | ||

| Miscellaneous reinsurance accepted business | 39.0% | 14.0% |

- 31/12/2006

Long-term insurance capital requirement

INSPRU 1.1.80

See Notes

- 31/12/2006

Insurance death risk capital component

INSPRU 1.1.81

See Notes

- 31/12/2006

INSPRU 1.1.81A

See Notes

- 31/12/2006

INSPRU 1.1.82

See Notes

- 31/12/2006

INSPRU 1.1.83

See Notes

- 31/12/2006

INSPRU 1.1.83A

See Notes

- 31/12/2006

INSPRU 1.1.84

See Notes

- 31/12/2006

INSPRU 1.1.84A

See Notes

- 31/12/2006

Insurance health risk and life protection reinsurance capital component

INSPRU 1.1.85

See Notes

- 31/12/2006

INSPRU 1.1.86

See Notes

- 31/12/2006

INSPRU 1.1.87

See Notes

- 31/12/2006

Insurance expense risk capital component

INSPRU 1.1.88

See Notes

- 31/12/2006

INSPRU 1.1.88A

See Notes

- 31/12/2006

Insurance market risk capital component

INSPRU 1.1.89

See Notes

- 31/12/2006

Adjusted mathematical reserves

INSPRU 1.1.89A

See Notes

- 31/12/2006

INSPRU 1.1.90

See Notes

- 31/12/2006

INSPRU 1.1.91

See Notes

- 31/12/2006

INSPRU 1.1.92

See Notes

- 31/12/2006

Insurance special purpose vehicles

INSPRU 1.1.92A

See Notes

- 31/12/2006

INSPRU 1.1.92B

See Notes

- 31/12/2006

Application of INSPRU 1.1 to Lloyd's

INSPRU 1.1.93

See Notes

- 31/12/2006

INSPRU 1.1.94

See Notes

- 31/12/2006

INSPRU 1.1.95

See Notes

- 31/12/2006

INSPRU 1.1.96

See Notes

- 31/12/2006

INSPRU 1.2

Mathematical reserves

- 31/12/2006

Application

INSPRU 1.2.1

See Notes

- 31/12/2006

Purpose

INSPRU 1.2.2

See Notes

- 31/12/2006

INSPRU 1.2.3

See Notes

- 31/12/2006

INSPRU 1.2.4

See Notes

- 31/12/2006

INSPRU 1.2.5

See Notes

- 31/12/2006

INSPRU 1.2.6

See Notes

- 31/12/2006

Basic valuation method

INSPRU 1.2.7

See Notes

- 31/12/2006

INSPRU 1.2.8

See Notes

- 31/12/2006

INSPRU 1.2.9

See Notes

- 31/12/2006

Methods and assumptions

INSPRU 1.2.10

See Notes

- 31/12/2006

INSPRU 1.2.11

See Notes

- 31/12/2006

INSPRU 1.2.12

See Notes

- 31/12/2006

Margins for adverse deviation

INSPRU 1.2.13

See Notes

- 31/12/2006

INSPRU 1.2.14

See Notes

- 31/12/2006

INSPRU 1.2.15

See Notes

- 31/12/2006

INSPRU 1.2.16

See Notes

The margin for adverse deviation of a risk should generally be greater than or equal to the relevant market price for that risk.

- 31/12/2006

INSPRU 1.2.17

See Notes

- 31/12/2006

INSPRU 1.2.18

See Notes

- 31/12/2006

INSPRU 1.2.19

See Notes

The rules and guidance on margins for adverse deviation in respect of future investment returns, which are also required in the calculation of mathematical reserves, are set out in INSPRU 3.1.28 R to INSPRU 3.1.48 G.

- 31/12/2006

Record keeping

INSPRU 1.2.20

See Notes

- 31/12/2006

INSPRU 1.2.21

See Notes

- 31/12/2006

Valuation of individual contracts

INSPRU 1.2.22

See Notes

- 31/12/2006

INSPRU 1.2.23

See Notes

- 31/12/2006

Negative mathematical reserves

INSPRU 1.2.24

See Notes

- 31/12/2006

INSPRU 1.2.25

See Notes

- 31/12/2006

Avoidance of future valuation strain

INSPRU 1.2.26

See Notes

- 31/12/2006

INSPRU 1.2.27

See Notes

- 31/12/2006

Cash flows to be valued

INSPRU 1.2.28

See Notes

- 31/12/2006

INSPRU 1.2.28A

See Notes

- 31/12/2006

INSPRU 1.2.29

See Notes

- 31/12/2006

INSPRU 1.2.30

See Notes

- 31/12/2006

INSPRU 1.2.31

See Notes

- 31/12/2006

Valuation assumptions: detailed rules and guidance

INSPRU 1.2.32

See Notes

- 31/12/2006

Valuation rates of interest

INSPRU 1.2.33

See Notes

- 31/12/2006

INSPRU 1.2.34

See Notes

- 31/12/2006

Future premiums

INSPRU 1.2.35

See Notes

- 31/12/2006

INSPRU 1.2.36

See Notes

- 31/12/2006

Future premiums: firms reporting only on a regulatory basis

INSPRU 1.2.37

See Notes

- 31/12/2006

INSPRU 1.2.38

See Notes

- 31/12/2006

INSPRU 1.2.39

See Notes

- 31/12/2006

INSPRU 1.2.40

See Notes

- 31/12/2006

INSPRU 1.2.41

See Notes

- 31/12/2006

INSPRU 1.2.42

See Notes

- 31/12/2006

Future net premiums: adjustment for deferred acquisition costs

INSPRU 1.2.43

See Notes

- 31/12/2006

INSPRU 1.2.44

See Notes

- 31/12/2006

INSPRU 1.2.45

See Notes

- 31/12/2006

Future premiums: firms also reporting with-profits insurance liabilities on a realistic basis

INSPRU 1.2.46

See Notes

- 31/12/2006

INSPRU 1.2.47

See Notes

- 31/12/2006

Future premiums: accumulating with-profits policies

INSPRU 1.2.48

See Notes

- 31/12/2006

INSPRU 1.2.49

See Notes

- 31/12/2006

Expenses

INSPRU 1.2.50

See Notes

- 31/12/2006

INSPRU 1.2.51

See Notes

- 31/12/2006

INSPRU 1.2.52

See Notes

- 31/12/2006

INSPRU 1.2.53

See Notes

- 31/12/2006

INSPRU 1.2.54

See Notes

- 31/12/2006

INSPRU 1.2.54A

See Notes

- 31/12/2006

INSPRU 1.2.54B

See Notes

- 31/12/2006

INSPRU 1.2.55

See Notes

- 31/12/2006

INSPRU 1.2.56

See Notes

- 31/12/2006

INSPRU 1.2.57

See Notes

- 31/12/2006

INSPRU 1.2.58

See Notes

- 31/12/2006

Mortality and Morbidity

INSPRU 1.2.59

See Notes

- 31/12/2006

INSPRU 1.2.60

See Notes

- 31/12/2006

INSPRU 1.2.61

See Notes

- 31/12/2006

Options

INSPRU 1.2.62

See Notes

- 31/12/2006

INSPRU 1.2.62A

See Notes

- 31/12/2006

INSPRU 1.2.63

See Notes

- 31/12/2006

INSPRU 1.2.64

See Notes

- 31/12/2006

INSPRU 1.2.65

See Notes

- 31/12/2006

INSPRU 1.2.66

See Notes

- 31/12/2006

INSPRU 1.2.67

See Notes

- 31/12/2006

INSPRU 1.2.68

See Notes

- 31/12/2006

INSPRU 1.2.69

See Notes

- 31/12/2006

INSPRU 1.2.70

See Notes

- 31/12/2006

INSPRU 1.2.71

See Notes

- 31/12/2006

INSPRU 1.2.72

See Notes

- 31/12/2006

Persistency assumptions

INSPRU 1.2.73

See Notes

- 31/12/2006

INSPRU 1.2.74

See Notes

- 31/12/2006

INSPRU 1.2.75

See Notes

- 31/12/2006

INSPRU 1.2.76

See Notes

- 31/12/2006

INSPRU 1.2.77

See Notes

- 31/12/2006

Reinsurance

INSPRU 1.2.77A

See Notes

- 31/12/2006

INSPRU 1.2.78

See Notes

- 31/12/2006

INSPRU 1.2.79

See Notes

- 31/12/2006

INSPRU 1.2.80

See Notes

- 31/12/2006

INSPRU 1.2.81

See Notes

- 31/12/2006

INSPRU 1.2.82

See Notes

- 31/12/2006

INSPRU 1.2.83

See Notes

- 31/12/2006

INSPRU 1.2.84

See Notes

- 31/12/2006

INSPRU 1.2.85

See Notes

- 31/12/2006

INSPRU 1.2.86

See Notes

- 31/12/2006

INSPRU 1.2.87

See Notes

- 31/12/2006

INSPRU 1.2.88

See Notes

- 31/12/2006

INSPRU 1.2.89

See Notes

- 31/12/2006

Application of INSPRU 1.2 to Lloyd's

INSPRU 1.2.92

See Notes

- 31/12/2006

Approved reinsurance to close

INSPRU 1.2.93

See Notes

- 31/12/2006

INSPRU 1.3

With-profits insurance capital component

- 31/12/2006

Application

INSPRU 1.3.1

See Notes

- 31/12/2006

INSPRU 1.3.2

See Notes

- 31/12/2006

Purpose

INSPRU 1.3.3

See Notes

- 31/12/2006

INSPRU 1.3.4

See Notes

- 31/12/2006

INSPRU 1.3.5

See Notes

- 31/12/2006

Main requirements

INSPRU 1.3.6

See Notes

- 31/12/2006

INSPRU 1.3.7

See Notes

- 31/12/2006

INSPRU 1.3.7A

See Notes

- 31/12/2006

INSPRU 1.3.8

See Notes

- 31/12/2006

INSPRU 1.3.9

See Notes

- 31/12/2006

General

Definitions

INSPRU 1.3.10

See Notes

- 31/12/2006

INSPRU 1.3.11

See Notes

- 31/12/2006

INSPRU 1.3.12

See Notes

- 31/12/2006

INSPRU 1.3.13

See Notes

- 31/12/2006

INSPRU 1.3.14

See Notes

- 31/12/2006

INSPRU 1.3.15

See Notes

- 31/12/2006

INSPRU 1.3.16

See Notes

- 31/12/2006

Record keeping

INSPRU 1.3.17

See Notes

- 31/12/2006

INSPRU 1.3.18

See Notes

- 31/12/2006

INSPRU 1.3.19

See Notes

- 31/12/2006

INSPRU 1.3.20

See Notes

- 31/12/2006

General principles for allocating aggregate amounts

INSPRU 1.3.21

See Notes

- 31/12/2006

INSPRU 1.3.22

See Notes

- 31/12/2006

Calculation of regulatory excess capital

INSPRU 1.3.23

See Notes

- 31/12/2006

Regulatory value of assets

INSPRU 1.3.24

See Notes

- 31/12/2006

INSPRU 1.3.25

See Notes

- 31/12/2006

INSPRU 1.3.26

See Notes

- 31/12/2006

INSPRU 1.3.27

See Notes

- 31/12/2006

INSPRU 1.3.28

See Notes

- 31/12/2006

Regulatory value of liabilities

INSPRU 1.3.29

See Notes

- 31/12/2006

INSPRU 1.3.30

See Notes

- 31/12/2006

INSPRU 1.3.31

See Notes

as disclosed at lines 49 and 12 respectively of the appropriate Form 14 ('Long-term business liabilities and margins') for that fund as part of the Annual Returns required to be deposited with the FSA under IPRU(INS) rule 9.6R(1).

- 31/12/2006

Calculation of realistic excess capital

INSPRU 1.3.32

See Notes

- 31/12/2006

Realistic value of assets

INSPRU 1.3.33

See Notes

- 31/12/2006

INSPRU 1.3.34

See Notes

- 31/12/2006

INSPRU 1.3.35

See Notes

- 31/12/2006

INSPRU 1.3.36

See Notes

- 31/12/2006

INSPRU 1.3.37

See Notes

- 31/12/2006

INSPRU 1.3.38

See Notes

- 31/12/2006

INSPRU 1.3.39

See Notes

- 31/12/2006

INSPRU 1.3.39A

See Notes

- 31/12/2006

INSPRU 1.3.39B

See Notes

- 31/12/2006

Realistic value of liabilities: general

INSPRU 1.3.40

See Notes

- 31/12/2006

INSPRU 1.3.41

See Notes

- 31/12/2006

INSPRU 1.3.42

See Notes

- 31/12/2006

Risk capital margin

INSPRU 1.3.43

See Notes

- 31/12/2006

INSPRU 1.3.44

See Notes

- 31/12/2006

INSPRU 1.3.45

See Notes

- 31/12/2006

INSPRU 1.3.46

See Notes

- 31/12/2006

INSPRU 1.3.47

See Notes

arising from the effects of market risk, credit risk and persistency risk. Other risks are not explicitly addressed by the risk capital margin.

- 31/12/2006

INSPRU 1.3.48

See Notes

- 31/12/2006

INSPRU 1.3.49

See Notes

- 31/12/2006

INSPRU 1.3.50

See Notes

- 31/12/2006

INSPRU 1.3.51

See Notes

- 31/12/2006

INSPRU 1.3.51A

See Notes

- 31/12/2006

Management actions

INSPRU 1.3.52

See Notes

- 31/12/2006

INSPRU 1.3.53

See Notes

- 31/12/2006

INSPRU 1.3.54

See Notes

- 31/12/2006

INSPRU 1.3.55

See Notes

- 31/12/2006

INSPRU 1.3.56

See Notes

- 31/12/2006

INSPRU 1.3.57

See Notes

- 31/12/2006

Policyholder actions

INSPRU 1.3.58

See Notes

- 31/12/2006

INSPRU 1.3.59

See Notes

- 31/12/2006

INSPRU 1.3.60

See Notes

- 31/12/2006

INSPRU 1.3.61

See Notes

- 31/12/2006

Market risk scenario

INSPRU 1.3.62

See Notes

- 31/12/2006

INSPRU 1.3.63

See Notes

- 31/12/2006

INSPRU 1.3.63A

See Notes

- 31/12/2006

INSPRU 1.3.64

See Notes

- 31/12/2006

INSPRU 1.3.65

See Notes

- 31/12/2006

INSPRU 1.3.67

See Notes

- 31/12/2006

Market risk scenario for exposures to UK assets and certain non-UK assets

INSPRU 1.3.68

See Notes

- 31/12/2006

INSPRU 1.3.69

See Notes

- 31/12/2006

INSPRU 1.3.70

See Notes

- 31/12/2006

Equity market adjustment ratio

INSPRU 1.3.71

See Notes

- 31/12/2006

INSPRU 1.3.72

See Notes

- 31/12/2006

Market risk scenario for exposures to other non-UK assets

INSPRU 1.3.73

See Notes

- 31/12/2006

INSPRU 1.3.74

See Notes

- 31/12/2006

INSPRU 1.3.75

See Notes

- 31/12/2006

INSPRU 1.3.76

See Notes

- 31/12/2006

Credit risk scenarios

General

INSPRU 1.3.77

See Notes

- 31/12/2006

INSPRU 1.3.78

See Notes

- 31/12/2006

INSPRU 1.3.79

See Notes

- 31/12/2006

INSPRU 1.3.80

See Notes

- 31/12/2006

INSPRU 1.3.81

See Notes

- 31/12/2006

INSPRU 1.3.82

See Notes

- 31/12/2006

INSPRU 1.3.83

See Notes

- 31/12/2006

Spread stresses to be assumed for bonds and debt

INSPRU 1.3.84

See Notes

- 31/12/2006

INSPRU 1.3.85

See Notes

- 31/12/2006

INSPRU 1.3.86

See Notes

- 31/12/2006

INSPRU 1.3.87

See Notes

- 31/12/2006

INSPRU 1.3.88

See Notes

- 31/12/2006

INSPRU 1.3.89

See Notes

- 31/12/2006

Table : Listed rating agencies, credit rating descriptions, spread factors

INSPRU 1.3.90

See Notes

| Credit Rating Description | Listed rating agencies | Spread Factor | |||

| A. M. Best Company | Fitch Ratings | Moodys Investors Service | Standard & Poors Corporation | ||

| Exceptional or extremely strong | aaa | AAA | Aaa | AAA | 3.00 |

| Very strong | aa | AA | Aa | AA | 5.25 |

| Strong | a | A | A | A | 6.75 |

| Adequate | bbb | BBB | Baa | BBB | 9.25 |

| Speculative or less vulnerable | bb | BB | Ba | BB | 15.00 |

| Very speculative or more vulnerable | B | B | B | B | 24.00 |

| Highly speculative or very vulnerable | Below B | Below B | Below B | Below B | 24.00 |

- 31/12/2006

INSPRU 1.3.91

See Notes

- 31/12/2006

INSPRU 1.3.92

See Notes

- 31/12/2006

INSPRU 1.3.93

See Notes

- 31/12/2006

Credit risk scenario for reinsurance

INSPRU 1.3.94

See Notes

- 31/12/2006

INSPRU 1.3.95

See Notes

- 31/12/2006

INSPRU 1.3.96

See Notes

- 31/12/2006

INSPRU 1.3.97

See Notes

| Financial Strength Description | A. M. Best Company | Fitch Ratings | Moodys Investors Service | Standard & Poors Corporation | Spread Factor |

| Superior, extremely strong | A++ | AAA | Aaa | AAA | 3.00 |

| Superior, very strong | A+ | AA | Aa | AA | 5.25 |

| Excellent or strong | A, A- | A | A | A | 6.75 |

| Good | B++, B+ | BBB | Baa | BBB | 9.25 |

| Fair, marginal | B, B- | BB | Ba | BB | 15.00 |

| Marginal, weak | C++, C+ | B | B | B | 24.00 |

| Unrated or very weak | Unrated or below C++, C+ | Unrated or below B | Unrated or below B | Unrated or below B | 24.00 |

- 31/12/2006

Credit risk scenario for other exposures (including any derivative or quasi-derivative)

INSPRU 1.3.98

See Notes

- 31/12/2006

INSPRU 1.3.99

See Notes

- 31/12/2006

Persistency risk scenario

INSPRU 1.3.100

See Notes

- 31/12/2006

INSPRU 1.3.101

See Notes

- 31/12/2006

INSPRU 1.3.102

See Notes

- 31/12/2006

INSPRU 1.3.103

See Notes

- 31/12/2006

Realistic value of liabilities: detailed provisions

INSPRU 1.3.104

See Notes

- 31/12/2006

Methods and assumptions: general

INSPRU 1.3.105

See Notes

- 31/12/2006

INSPRU 1.3.106

See Notes

- 31/12/2006

INSPRU 1.3.107

See Notes

- 31/12/2006

INSPRU 1.3.108

See Notes

- 31/12/2006

Valuation of contracts: General

INSPRU 1.3.109

See Notes

- 31/12/2006

INSPRU 1.3.110

See Notes

- 31/12/2006

INSPRU 1.3.111

See Notes

- 31/12/2006

INSPRU 1.3.112

See Notes

- 31/12/2006

INSPRU 1.3.113

See Notes

- 31/12/2006

INSPRU 1.3.114

See Notes

- 31/12/2006

INSPRU 1.3.115

See Notes

- 31/12/2006

With-profits benefits reserve

INSPRU 1.3.116

See Notes

- 31/12/2006

INSPRU 1.3.117

See Notes

- 31/12/2006

Retrospective method

INSPRU 1.3.118

See Notes

- 31/12/2006

INSPRU 1.3.119

See Notes

- 31/12/2006

INSPRU 1.3.120

See Notes

- 31/12/2006

INSPRU 1.3.121

See Notes

- 31/12/2006

INSPRU 1.3.122

See Notes

- 31/12/2006

INSPRU 1.3.123

See Notes

- 31/12/2006

INSPRU 1.3.124

See Notes

- 31/12/2006

INSPRU 1.3.125

See Notes

- 31/12/2006

INSPRU 1.3.126

See Notes

- 31/12/2006

INSPRU 1.3.127

See Notes

- 31/12/2006

Prospective method

INSPRU 1.3.128

See Notes

- 31/12/2006

INSPRU 1.3.129

See Notes

- 31/12/2006

INSPRU 1.3.130

See Notes

- 31/12/2006

INSPRU 1.3.131

See Notes

- 31/12/2006

INSPRU 1.3.132

See Notes

- 31/12/2006

INSPRU 1.3.133

See Notes

- 31/12/2006

INSPRU 1.3.134

See Notes

- 31/12/2006

INSPRU 1.3.135

See Notes

- 31/12/2006

Future policy related liabilities

INSPRU 1.3.136

See Notes

INSPRU 1.3.137 R lists the future policy related liabilities for a with-profits fund that form part of a firm'srealistic value of liabilities in INSPRU 1.3.40 R. Detailed rules and guidance relating to particular types of liability and asset are set out in INSPRU 1.3.139 R to INSPRU 1.3.168 G. These are followed by rules and guidance that deal with certain aspects of several liabilities (that is, liabilities relating to guarantees, options and smoothing):

- 31/12/2006

INSPRU 1.3.137

See Notes

- 31/12/2006

INSPRU 1.3.138

See Notes

- 31/12/2006

Past miscellaneous surplus (or deficit) planned to be attributed to the with-profits benefits reserve

INSPRU 1.3.139

See Notes

- 31/12/2006

INSPRU 1.3.140

See Notes

- 31/12/2006

Planned enhancements to the with-profits benefits reserve

INSPRU 1.3.141

See Notes

- 31/12/2006

INSPRU 1.3.142

See Notes

- 31/12/2006

INSPRU 1.3.143

See Notes

- 31/12/2006

Planned deductions for the costs of guarantees, options and smoothing from the with-profits benefits reserve

INSPRU 1.3.144

See Notes

- 31/12/2006

INSPRU 1.3.145

See Notes

- 31/12/2006

Planned deductions for other costs deemed chargeable to the with-profits benefits reserve

INSPRU 1.3.146

See Notes

- 31/12/2006

INSPRU 1.3.147

See Notes

- 31/12/2006

Future costs of contractual guarantees (other than financial options)

INSPRU 1.3.148

See Notes

- 31/12/2006

INSPRU 1.3.149

See Notes

- 31/12/2006

INSPRU 1.3.150

See Notes

- 31/12/2006

INSPRU 1.3.151

See Notes

- 31/12/2006

INSPRU 1.3.152

See Notes

- 31/12/2006

INSPRU 1.3.153

See Notes

- 31/12/2006

Future costs of non-contractual commitments

INSPRU 1.3.154

See Notes

- 31/12/2006

INSPRU 1.3.155

See Notes

- 31/12/2006

Future costs of financial options

INSPRU 1.3.156

See Notes

- 31/12/2006

INSPRU 1.3.157

See Notes

- 31/12/2006

Future costs of smoothing

INSPRU 1.3.158

See Notes

- 31/12/2006

INSPRU 1.3.159

See Notes

- 31/12/2006

INSPRU 1.3.160

See Notes

- 31/12/2006

INSPRU 1.3.161

See Notes

- 31/12/2006

Financing costs

INSPRU 1.3.162

See Notes

- 31/12/2006

INSPRU 1.3.163

See Notes

- 31/12/2006

INSPRU 1.3.164

See Notes

- 31/12/2006

Other long-term insurance liabilities

INSPRU 1.3.165

See Notes

- 31/12/2006

INSPRU 1.3.166

See Notes

- 31/12/2006

INSPRU 1.3.167

See Notes

- 31/12/2006

INSPRU 1.3.168

See Notes

- 31/12/2006

Valuing the costs of guarantees, options and smoothing

INSPRU 1.3.169

See Notes

- 31/12/2006

INSPRU 1.3.170

See Notes

- 31/12/2006

INSPRU 1.3.171

See Notes

- 31/12/2006

INSPRU 1.3.172

See Notes

- 31/12/2006

INSPRU 1.3.173

See Notes

- 31/12/2006

INSPRU 1.3.174

See Notes

- 31/12/2006

INSPRU 1.3.175

See Notes

- 31/12/2006

Stochastic approach

INSPRU 1.3.176

See Notes

- 31/12/2006

INSPRU 1.3.177

See Notes

- 31/12/2006

INSPRU 1.3.178

See Notes

- 31/12/2006

INSPRU 1.3.179

See Notes

- 31/12/2006

INSPRU 1.3.180

See Notes

- 31/12/2006

Deterministic approach

INSPRU 1.3.181

See Notes

- 31/12/2006

INSPRU 1.3.182

See Notes

- 31/12/2006

INSPRU 1.3.183

See Notes

- 31/12/2006

INSPRU 1.3.184

See Notes

- 31/12/2006

Management and policyholder actions

INSPRU 1.3.185

See Notes

- 31/12/2006

INSPRU 1.3.186

See Notes

- 31/12/2006

Treatment of surplus on guarantees, options and smoothing

INSPRU 1.3.187

See Notes

- 31/12/2006

INSPRU 1.3.188

See Notes

- 31/12/2006

INSPRU 1.3.189

See Notes

- 31/12/2006

Realistic current liabilities

INSPRU 1.3.190

See Notes

- 31/12/2006

INSPRU 1.3.191

See Notes

- 31/12/2006

INSPRU 1.4

Equalisation provisions

- 31/12/2006

Application

INSPRU 1.4.1

See Notes

- 31/12/2006

INSPRU 1.4.2

See Notes

- 31/12/2006

INSPRU 1.4.3

See Notes

- 31/12/2006

Purpose

INSPRU 1.4.4

See Notes

- 31/12/2006

INSPRU 1.4.5

See Notes

- 31/12/2006

INSPRU 1.4.6

See Notes

- 31/12/2006

INSPRU 1.4.7

See Notes

| Table: Scope of insurance business to be included in calculations | ||||

| Type Of Firm | Credit Equalisation Provision | Non Credit Equalisation Provision | ||

| Threshold in INSPRU 1.4.4 G | Provision in INSPRU 1.4.43 R | Threshold in INSPRU 1.4.18R (2) and provision in INSPRU 1.4.17 R | ||

| UK insurer | World-wide | World-wide | World-wide | |

| Pure reinsurer with head office outside United Kingdom | UK | World-wide | UK | |

| Pure reinsurer with head office in United Kingdom | World-wide | World-wide | World-wide | |

| Non-EEA direct insurers | EEA-deposit insurer | UK | UK | UK |

| Swiss general insurer | UK | UK | UK | |

| UK-deposit insurer | All EEA | World-wide | UK | |

| All other non-EEA direct insurers | UK | World-wide | UK | |

- 31/12/2006

INSPRU 1.4.8

See Notes

- 31/12/2006

INSPRU 1.4.9

See Notes

- 31/12/2006

INSPRU 1.4.10

See Notes

- 31/12/2006

Non-credit equalisation provision

INSPRU 1.4.11

See Notes

- 31/12/2006

INSPRU 1.4.12

See Notes

| Insurance Business Grouping | General Insurance Contracts | |

| A | Contracts of insurance which fall within general insurance businessclasses 4, 8 or 9, other than: | |

| (a) | contracts of insurance under non-proportional reinsurance treaties; and | |

| (b) | contracts of insurance against nuclear risks | |

| B | Contracts of insurance which fall within general insurance businessclass 16(a), other than: | |

| (a) | contracts of insurance under non-proportional reinsurance treaties; and | |

| (b) | contracts of insurance against nuclear risks | |

| C | Contracts of insurance which fall within general insurance business classes 5, 6, 11 or 12, other than: | |

| (a) | contracts of insurance against nuclear risks; and | |

| (b) | reinsurance contracts corresponding to contracts in (a). | |

| D | Contracts of insurance against nuclear risks. | |

| E | Contracts of insurance under non-proportional reinsurance treaties and which fall within general insurance business classes 4, 8, 9 or 16(a) other than contracts of insurance against nuclear risks. | |

- 31/12/2006

INSPRU 1.4.13

See Notes

- 31/12/2006

INSPRU 1.4.14

See Notes

- 31/12/2006

INSPRU 1.4.15

See Notes

- 31/12/2006

INSPRU 1.4.16

See Notes

- 31/12/2006

Requirement to maintain non-credit equalisation provision

INSPRU 1.4.17

See Notes

- 31/12/2006

INSPRU 1.4.18

See Notes

- 31/12/2006

INSPRU 1.4.19

See Notes

- 31/12/2006

Calculating the amount of the provision

INSPRU 1.4.20

See Notes

- 31/12/2006

INSPRU 1.4.21

See Notes

- 31/12/2006

INSPRU 1.4.22

See Notes

- 31/12/2006

INSPRU 1.4.23

See Notes

- 31/12/2006

The calculation: the maximum provision

INSPRU 1.4.24

See Notes

- 31/12/2006

INSPRU 1.4.25

See Notes

| Insurance Business Grouping | Percentage of average annualised net written premiums |

| A | 20 |

| B | 20 |

| C | 40 |

| D | 600 |

| E | 75 |

- 31/12/2006

The calculation: provisional transfers-in

INSPRU 1.4.26

See Notes

- 31/12/2006

INSPRU 1.4.27

See Notes

| Insurance Business Grouping | Percentage of net written premiums |

| A | 3 |

| B | 3 |

| C | 6 |

| D | 75 |

| E | 11 |

- 31/12/2006

INSPRU 1.4.28

See Notes

- 31/12/2006

The calculation: provisional transfers-out

INSPRU 1.4.29

See Notes

- 31/12/2006

INSPRU 1.4.30

See Notes

- 31/12/2006

INSPRU 1.4.31

See Notes

| Insurance Business Grouping | Percentage of net written premiums |

| A | 72.5 |

| B | 72.5 |

| C | 95 |

| D | 25 |

| E | 100 |

- 31/12/2006

Adjustments to calculations

INSPRU 1.4.32

See Notes

- 31/12/2006

INSPRU 1.4.33

See Notes

- 31/12/2006

Transfers of business to the firm

INSPRU 1.4.34

See Notes

- 31/12/2006

INSPRU 1.4.35

See Notes

- 31/12/2006

INSPRU 1.4.36

See Notes

- 31/12/2006

INSPRU 1.4.37

See Notes

- 31/12/2006

Credit equalisation provisions

INSPRU 1.4.38

See Notes

INSPRU 1.4.39 R to INSPRU 1.4.47 G apply to any firm which carries on the business of effecting or carrying out general insurance contracts falling within general insurance businessclass 14 (which business is referred to in INSPRU 1.4 as "credit insurance business"), unless it is:

- 31/12/2006

INSPRU 1.4.39

See Notes

- 31/12/2006

INSPRU 1.4.40

See Notes

- 31/12/2006

INSPRU 1.4.41

See Notes

- 31/12/2006

INSPRU 1.4.42

See Notes

- 31/12/2006

Requirement to maintain credit equalisation provision

INSPRU 1.4.43

See Notes

- 31/12/2006

INSPRU 1.4.44

See Notes

- 31/12/2006

Calculating the amount of the provision

INSPRU 1.4.45

See Notes

- 31/12/2006

INSPRU 1.4.46

See Notes

- 31/12/2006

INSPRU 1.4.47

See Notes

- 31/12/2006

Euro conversion

INSPRU 1.4.48

See Notes

- 31/12/2006

Application of INSPRU 1.4 to Lloyd's

INSPRU 1.4.49

See Notes

- 31/12/2006

INSPRU 1.4.50

See Notes

- 31/12/2006

INSPRU 1.4.51

See Notes

- 31/12/2006

INSPRU 1.5

Internal-contagion risk

- 31/12/2006

Application

INSPRU 1.5.1

See Notes

- 31/12/2006

INSPRU 1.5.2

See Notes

- 31/12/2006

INSPRU 1.5.3

See Notes

- 31/12/2006

INSPRU 1.5.4

See Notes

- 31/12/2006

INSPRU 1.5.5

See Notes

- 31/12/2006

INSPRU 1.5.6

See Notes

- 31/12/2006

INSPRU 1.5.7

See Notes

- 31/12/2006

Purpose

INSPRU 1.5.8

See Notes

- 31/12/2006

INSPRU 1.5.9

See Notes

- 31/12/2006

INSPRU 1.5.10

See Notes

- 31/12/2006

INSPRU 1.5.11

See Notes

- 31/12/2006

INSPRU 1.5.12

See Notes

- 31/12/2006

Requirements: Non-insurance activities

Restriction of business

INSPRU 1.5.13

See Notes

- 31/12/2006

INSPRU 1.5.13A

See Notes

- 31/12/2006

INSPRU 1.5.13B

See Notes

- 31/12/2006

Financial limitation of non-insurance activities

INSPRU 1.5.14

See Notes

- 31/12/2006

INSPRU 1.5.15

See Notes

- 31/12/2006

Requirements: long-term insurance business

INSPRU 1.5.16

See Notes

- 31/12/2006

Permissions not to include both types of insurance

INSPRU 1.5.17

See Notes

- 31/12/2006

Separately identify and maintain long term insurance assets

INSPRU 1.5.18

See Notes

- 31/12/2006

INSPRU 1.5.19

See Notes

- 31/12/2006

INSPRU 1.5.20

See Notes

- 31/12/2006

INSPRU 1.5.21

See Notes

- 31/12/2006

INSPRU 1.5.22

See Notes

- 31/12/2006

INSPRU 1.5.23

See Notes

- 31/12/2006

INSPRU 1.5.24

See Notes

- 31/12/2006

INSPRU 1.5.25

See Notes

- 31/12/2006

INSPRU 1.5.26

See Notes

- 31/12/2006

INSPRU 1.5.27

See Notes

- 31/12/2006

INSPRU 1.5.28

See Notes

- 31/12/2006

INSPRU 1.5.29

See Notes

- 31/12/2006

Exclusive use of long-term insurance assets

INSPRU 1.5.30

See Notes

- 31/12/2006

INSPRU 1.5.31

See Notes

- 31/12/2006

INSPRU 1.5.32

See Notes

- 31/12/2006

Payment of financial penalties

INSPRU 1.5.33

See Notes

- 31/12/2006

INSPRU 1.5.34

See Notes

- 31/12/2006

Requirements: property-linked funds

INSPRU 1.5.35

See Notes

- 31/12/2006

INSPRU 1.5.36

See Notes

- 31/12/2006

INSPRU 1.5.37

See Notes

- 31/12/2006

Requirements: UK branches of certain non-EEA firms

INSPRU 1.5.38

See Notes

- 31/12/2006

INSPRU 1.5.39

See Notes

- 31/12/2006

INSPRU 1.5.40

See Notes

- 31/12/2006

Worldwide financial resources

INSPRU 1.5.41

See Notes

- 31/12/2006

UK or EEA MCR to be covered by admissible assets

INSPRU 1.5.42

See Notes

- 31/12/2006

INSPRU 1.5.43

See Notes

- 31/12/2006

INSPRU 1.5.44

See Notes

- 31/12/2006

INSPRU 1.5.45

See Notes

- 31/12/2006

INSPRU 1.5.46

See Notes

- 31/12/2006

INSPRU 1.5.47

See Notes

- 31/12/2006

Localisation of assets

INSPRU 1.5.48

See Notes

- 31/12/2006

INSPRU 1.5.49

See Notes

- 31/12/2006

INSPRU 1.5.50

See Notes

- 31/12/2006

INSPRU 1.5.51

See Notes

- 31/12/2006

INSPRU 1.5.52

See Notes

- 31/12/2006

INSPRU 1.5.53

See Notes

- 31/12/2006

Deposit of assets as security

INSPRU 1.5.54

See Notes

- 31/12/2006

INSPRU 1.5.55

See Notes

- 31/12/2006

Branch accounting records in the United Kingdom

INSPRU 1.5.56

See Notes

- 31/12/2006

INSPRU 1.5.57

See Notes

- 31/12/2006

Application of INSPRU 1.5 to Lloyd's

INSPRU 1.5.58

See Notes

- 31/12/2006

INSPRU 1.5.59

See Notes

- 31/12/2006

INSPRU 1.5.60

See Notes

- 31/12/2006

INSPRU 1.6

Insurance Special Purpose Vehicles

- 31/12/2006

Application and Purpose

INSPRU 1.6.1

See Notes

- 31/12/2006

INSPRU 1.6.2

See Notes

- 31/12/2006

INSPRU 1.6.3

See Notes

- 31/12/2006

INSPRU 1.6.4

See Notes

- 31/12/2006

Assets and liabilities

INSPRU 1.6.5

See Notes

- 31/12/2006

INSPRU 1.6.6

See Notes

- 31/12/2006

INSPRU 1.6.7

See Notes

- 31/12/2006

INSPRU 1.6.8

See Notes

- 31/12/2006

Contractual arrangements

INSPRU 1.6.9

See Notes

- 31/12/2006

INSPRU 1.6.10

See Notes

- 31/12/2006

INSPRU 1.6.11

See Notes

- 31/12/2006

INSPRU 1.6.12

See Notes

- 31/12/2006

Reinsurance with an ISPV

INSPRU 1.6.13

See Notes

unless it first obtains a waiver from the FSA . INSPRU 1.6.14 G to INSPRU 1.6.18 G set out the information which the FSA will expect to receive as part of the application for the waiver. Those paragraphs also set out the factors, in addition to the statutory tests under section 148 of the Act, to which the FSA will have regard in deciding:

- 31/12/2006

INSPRU 1.6.14

See Notes

- 31/12/2006

INSPRU 1.6.15

See Notes

- 31/12/2006

INSPRU 1.6.16

See Notes

- 31/12/2006

INSPRU 1.6.17

See Notes

- 31/12/2006

INSPRU 1.6.18

See Notes

- 31/12/2006

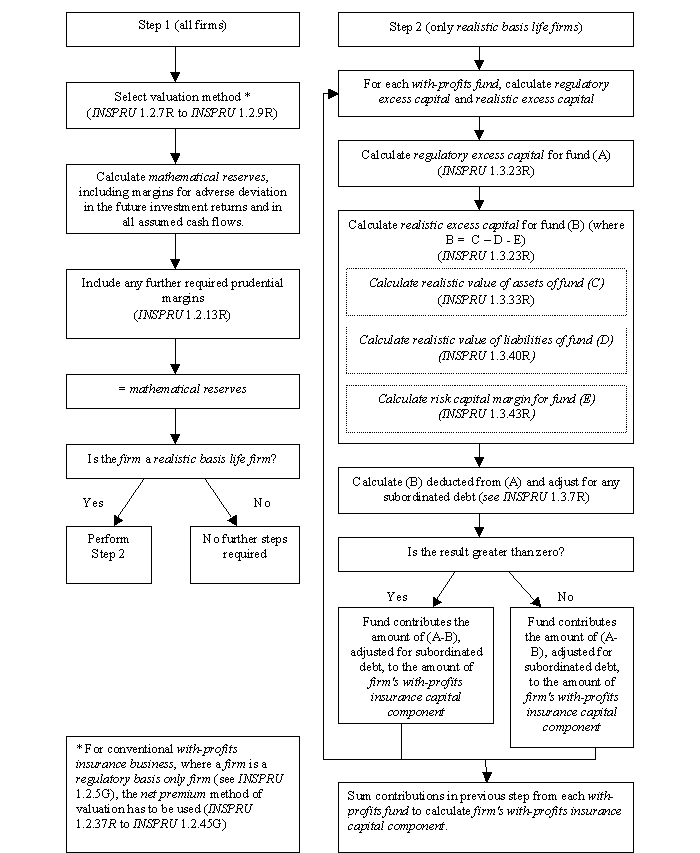

INSPRU 1 Annex 1

INSPRU 1.2 (Mathematical reserves) and INSPRU 1.3 (With-profits insurance capital component)

- 31/12/2006

See Notes

- 31/12/2006